engenders

One of the biggest winners during this earnings season has been Coinbase (NASDAQ:CURRENCY). Shares of the cryptocurrency platform have risen after the company Crushed Street estimates both on the top line and the bottom line. Although the first quarter of this The year was definitely much stronger than expected, there have been some worrying signs in the crypto space during the first half of Q2.

Coinbase reported net income of more than $736 million for the first quarter. While this was almost $430 million less than the prior year period, analysts were calling for the top figure to be around $650 million. This was the strongest quarter in the last three, as both transaction revenue and subscription/service revenue grew very well sequentially. The chart below shows the overall breakdown of revenue.

Quarterly Revenue Breakdown (Letter from the shareholder of the company)

Coinbase has also done a tremendous job of reducing his expense base. In the prior year period, transaction, sales and marketing expenses were more than 40% of net income. In the first quarter of 2023, the number nearly halved to around 22%. Other operating expenses, such as technology and overhead, have also been reduced significantly, with headcounts down more than 28.5% year-over-year. Even with more than $144 million in restructuring expenses recorded for the period, second-quarter net loss improved to less than $79 million from nearly $430 million a year earlier.

However, for the second quarter, things are not looking so rosy. Subscription and services revenue guidance is around $300 million, which would represent a decline of more than $60 million sequentially. Coinbase management noted in the letter to shareholders that USDC's average market cap in April was $31.7 billion, which was 23% lower than the first-quarter average of $41.3 billion. . USDC is a key driver of interest income, and the most recent data now has that market capitalization less than $30 billion and declining almost daily.

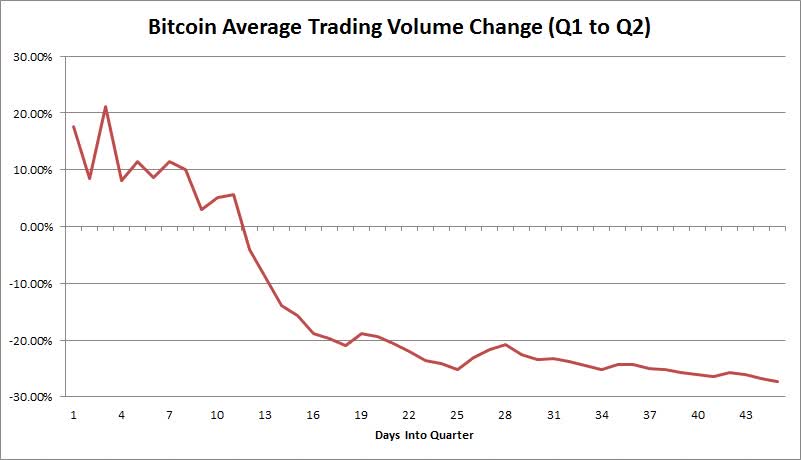

Management also stated that it generated approximately $110 million of transaction revenue in April as the volatility of crypto assets has decreased. In the first quarter, this segment of the business averaged about $125 million per month in revenue. There are reasons to be concerned here, for example, as Bitcoin trading volumes are not looking good at the moment. As the chart below shows, the average daily volume for the flagship cryptocurrency actually started during the first 11 days of the quarter, but has since worsened. The quarter-over-quarter decline was 24.54% through the 33rd (which would represent the day before Coinbase reported Q1), but that number is now over 27%.

Bitcoin daily volume (Yahoo)

I mention these recent trends because it looks like analyst estimates could be a little high right now. Considering what management guided, and the continued declines in both USDC market cap and Bitcoin volume since then, it appears that Coinbase is on track for a Q2 revenue impression in the low to low range. average of $600 million. Entering Tuesday, May 16, the mean analyst estimate for the quarter it was $686 million, which would certainly favor the bear camp.

Even though Coinbase shares are up about $5 above last week's high, they are still up 20% since the Q1 report. The 50-day moving average is only around $3 above current levels, and that key technical line could be one of the major resistances going forward. In the end, the second quarter trends so far for cryptocurrencies have not looked good, so investors at Coinbase should exercise some caution unless we see some of these key elements improve in the second half of the quarter.