case master

An epic squeeze pushed stocks higher this week, driven by a collection of factors that are unlikely to persist. As mentioned above, stocks are trading more in sync with bonds than at any time in recent memory, and this week saw a big move down in rates, starting Wednesday tomorrow.

The groundwork was laid Monday when the Treasury Announced would borrow just $776 billion of the previously estimated $852 billion in the fourth quarter. But the most significant news came Wednesday morning, before the Federal Reserve, when the Treasury driven its quarterly reimbursement at $112 billion versus estimates of $114 billion. Additionally, the Treasury announced a $48 billion 3-year auction, a $40 billion 10-year auction, and a $24 billion 30-year auction. This was less than the Dear All of 48 billion dollars, 41 billion dollars and 25 billion dollars, respectively. This caused ten- and 30-year rates to fall following the news.

Commercial view

Massive short on Treasury bonds

Remember that a huge short position has been built in 10- and 30-year Treasuries, and even what seems like the most insignificant news could cause market shocks, especially if it doesn't favor market positioning.

Bloomberg

Rates were not helped by Wednesday's disappointing ISM data or even Friday's employment data, which contributed to the decline in rates during the week. Additionally, it is also worth noting that last week there was No Afternoon Treasury bond auction, which has become a major source of volatility across markets. That will change this week with a 3-year auction on November 7, a 10-year auction on November 8, and a 30-year auction on November 9.

Treasury Auctions

Bloomberg

These auctions will be critical and could reintroduce a layer of volatility in the afternoon. The last 10-year auction did not go well, with a high yield rate of 4.61% against an issue yield of 4.592%, while indirect take rates fell to 60.3% from the 66.3% in September.

Bloomberg

The last 30-year auction was even worse than the 10-year auction. The 30-year auction lagged by almost four basis points, meaning it had a high yield rate of 4.837% versus an issue rate of 4.8%. Meanwhile, indirect acceptances rose to 65.1% compared to 64.5% in September. If this week's auctions go as poorly as those in recent months, bond market volatility seems likely to increase, and it's entirely possible that rates will begin to rise again.

Missing buyers

One of the reasons bond yields have soared is because the world's biggest bond buyers, central banks, have left. The combination of the central bank's balance sheet liquidation and the fact that it is no longer actively adding bonds to its holdings, along with a strong dollar, has decreased overall global liquidity levels, and that has had a direct impact on the price of US bonds, as noted by the decline in US 10-year Treasury futures. The decline in central bank balance sheets appears to be directly related to rising interest rates and falling prices.

Bloomberg

A trigger for the squeeze

Given the relationship between stock and bond prices, it's no surprise that this week's drop in interest rates was the direct trigger for stocks' rise. But rates were simply the trigger that drove the stock market up because once rates fell, it resulted in a gamma squeeze of epic proportions in the options markets.

Bloomberg

The S&P 500 was deep in negative gamma territory this week. According to GammaLabs, the S&P 500's net gamma was the lowest since the summer of 2022. Negative gamma environments produce high volatility and also tend to exacerbate moves in the market. When stock markets are in negative gamma, options traders buy or sell S&P 500 futures in the same direction as the market. When the market falls into negative gamma, market makers are sellers of futures, and when the market rises, market makers buy futures.

gamma laboratories

The combination of falling rates and the lack of Treasury auctions gave the stock markets a clear path to recover without interruption throughout the trading day, and that resulted in the large amount of buying we saw throughout the entire trading day. week. But the data now shows that the S&P 500 as of Friday has re-entered positive gamma, and that means market makers are sellers of strength and buyers of weakness. This will help alleviate volatility in the market and means that the speed of last week's significant gains is likely behind us.

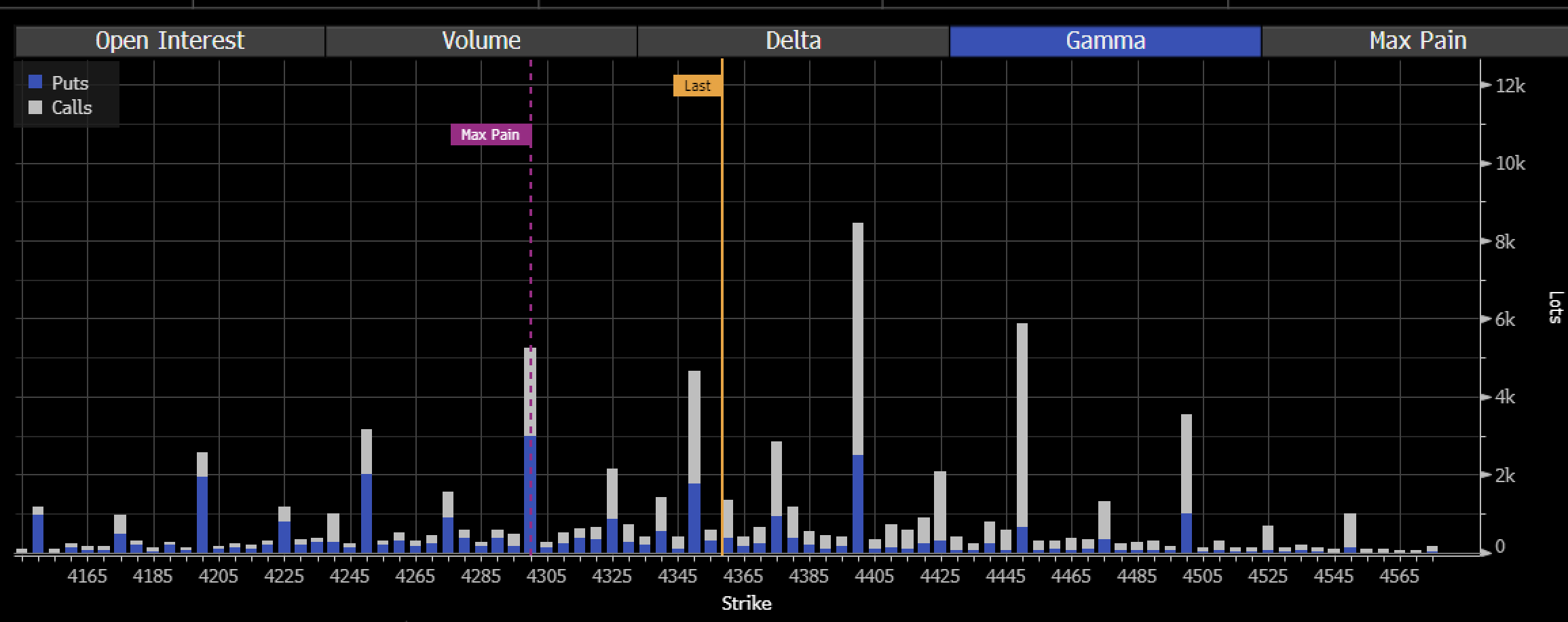

Meanwhile, the level on the S&P 500 with the most significant concentration of gamma and the level with the highest call gamma level is at 4,400. It will limit any further rise in the S&P 500 in the short term. unless The options market raises the call wall by purchasing options with higher strike prices. If the call wall does not rise higher, the options market will likely keep the index contained around 4,400 or lower. This is basically why the S&P 500 ran out of steam at the end of the day on Friday.

Bloomberg

Most of this week's move can be attributed to what happened on Wednesday morning and the positioning of the options market. It means that with the options market back in better balance and Treasury issuance resuming, it seems possible that the rally we saw last week will not advance with the same vigor.

Overall, the macro context shows that the economy is slowing, unemployment is rising and inflation is sticky. Additionally, earnings estimates for the fourth quarter and 2024 are steadily declining. The macroeconomic context of stagflation It will mean that rates on the back of the curve will stay the same or rise as the Treasury issues more debt, and that will prevent pent-up stocks from advancing much further, if at all.